Rethinking Europe’s capital markets strategy: Lessons from Sweden’s model

European households hold trillions in bank deposits while participation in capital markets remains underdeveloped. Sweden offers an alternative approach. ...

by Peter Vogel, Mara Catherine Harvey Published March 30, 2026 in Finance • 10 min read

From as young as three, children are taught how to spend. Pocket money, gifts from the tooth fairy, and vouchers for Christmas all arrive before a child is ever taught how to earn, creating a consumer-first mindset and contributing to declining financial literacy levels across the globe.

Financial literacy levels are faltering at a time when we need our children to be more financially capable, independent, and resilient than ever before. We are living in unprecedented times, set against the backdrop of the greatest wealth transfer in history. Trillions of dollars are moving downstream to the next generation, placing a magnified lens on what Eliza Filby calls an “inheritocracy culture” – a system where inherited wealth, connections, and privilege increasingly dictate outcomes, challenging the long‑held ideal of meritocracy.

Today’s children will inherit more wealth than any generation before them, yet student debts are spiraling, credit-card delinquency rates are double that of previous generations, and fast finance is negatively impacting financial capability across the board. The rising generations have been infantilized while being raised in a dystopian society where the construct of money is abstract, invisible, and associated with consumption rather than earning. They lack financial literacy, the core skills needed for handling delayed gratification, and suffer from both declining executive functioning and a severe bias in financial risk awareness due to digital-first learning.

With decades of experience in advising business-owning and wealthy families in financial parenting, we bring our pedagogical and practical experiences together to guide parents on how to raise financially capable and resilient children, no matter what their age or net worth.

Money skills must be acquired in the right order, and the foundation for financial literacy lies in creating a resources-first mindset and teaching children to earn before they spend.

Whether it’s money for birthdays or a gift from the tooth fairy, giving children the resources to spend before they learn how to earn is giving them a consumption-first mindset. If they are old enough to spend, they are old enough to earn. Every child can do some activity to contribute to something that you are willing to pay for, instead of simply gifting pocket money.

This is what successful UHNW and multi-generational enterprising families do incredibly well: they know their children need a resources-first logic and not a consumption-first logic, and they are very disciplined in imparting this. They will also mostly have, especially in the case of multi-generational families, examples from their family where the lack of financial literacy has led to unfavorable outcomes or behaviors, which is why they end up embedding this into the core of their next generation education and upbringing.

Less privileged households are also good at imparting a resources-first logic, but it often goes hand in hand with a scarcity mindset, as opposed to an abundance mindset. Limiting beliefs hinder children for life. Caught in the middle are the affluent households, who, for the love of their kids, afford them every wish and do not involve them in talking about money, because they can afford to provide for their children and are proud to do so. Smothering with love and avoiding money conversations are not a good strategy for raising money-smart kids.

“Ask yourself: when was the last time your children saw you earning or saving?”

Then the focus must shift to learning to save. So, you have the resources, but you are not going to rush out and give them all away.

Ask yourself: when was the last time your children saw you earning or saving?

The answer is likely never, as gone are the days when cash is brought home on pay day and stowed away in a piggy bank. Earning occurs purely digitally nowadays. Saving, too, is no longer visible to our children: it’s completely abstract, and yet, it is a core skill we need to teach our children, as it is going to be the most critical for their long-term success.

We often see toddlers throwing tantrums in supermarkets and it’s a microcosm of the issue we face today. They see their parents selectively taking things off a shelf and placing them into their trolley. The toddler wants to do the same, and when they are told not to, their frustration takes over because the exercise of making a list, discussing needs, wants, and prices has become completely invisible to them. If it’s invisible, a young child cannot learn it. They can only make sense out of what they see, which has little to do with planning and everything to do with execution.

The only visible part is the fast-finance part: a tap or a swipe, and you leave with your device in your hand. You haven’t given anything away, so money is not seen as a transaction: in the eyes of a young child, money is simply an action. The same way an item purchased online appears on a doorstep when it gets delivered – in a child’s eyes, we just “get” things, so the association of money with consumption is many times more visible than the effort put into acquiring the resources that we are consuming.

You must intentionally create time between earning and spending and creating that time is the act of saving.

The consumption mindset is exacerbated by the fact that the rising generation cannot deal with delayed gratification. It’s easier and instantly gratifying to buy a new handbag, rather than save for a house you may be able to afford in a decade.

You must intentionally create time between earning and spending and creating that time is the act of saving. Whenever you are in a store, and your child asks for something, or similarly, your teenager comes across an advert for something online, take a picture or screenshot and create a digital wish list. Emphasize that you have made a shopping list, you know what you’re in the store for, or you can outline your monthly priorities – involving them in an often invisible conversation – and then revisit it next time you are planning a shop or you have time and resources to prioritize that purchase.

Delayed gratification as a skill means putting time between having money and giving it away; when that child is older, they will feel comfortable and confident in investing their money and waiting until it bears its fruits.

It’s also important that in the process of creating responsible children and teaching philanthropy, we don’t teach generosity as a trade-off.

The next generation is bombarded with inescapable and unachievable illusions of wealth. Displays of lifestyle, such as designer bags or luxury cars on Instagram, are considered wealth by the younger generation. What they fail to understand is that this is consumption, and purchasing luxury items is a destruction of wealth. No one live-streams the 10 years of financial discipline required to afford or pay off a mortgage. Displays of lifestyle are a vicious trap that young people today are stuck in.

Financial capability is all about control: your child needs to be capable of setting their own priorities and not be swept away into consumer debt by impulse-driven purchases. Quality and morality matter too, and price is not the only dimension of spending. Part of becoming a self-reliant adult is understanding the social responsibilities that come with money. Call it moral wealth ownership, money choices, or simply being responsible.

This can mean teaching the importance of quality over quantity or having conversations with an older child about ensuring the clothing they want is made ethically. It translates into raising a generation of children who are going to become conscious consumers and investors with a fiduciary duty toward the planet, people, and society when they grow up.

It’s also important that in the process of creating responsible children and teaching philanthropy, we don’t teach generosity as a trade-off. It’s not either spending or saving or investing or giving money away to help others. Impact should be integrated into every money decision. They can spend money on a gift for somebody else, and that’s okay. But it shouldn’t be a trade-off between egotistic spending and generous, impactful spending.

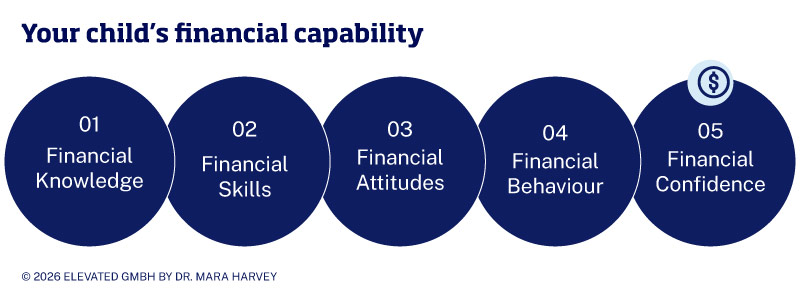

Money attitudes are formed between the ages of five and seven, so while much of our work over the years as an economist, professor, and advisor has been focused on educating adult investors on how to sustain and grow their wealth over generations, the advice often lands decades too late. That’s why this financial parenting framework was created. Its foundation is the framework for emotional intelligence, which is anchored in explicit and implicit learning, based on what we consciously teach our children and what our children see us do (or don’t see us do).

Financial knowledge and financial skills are explicit learning areas, the things you intentionally teach a child – the content, and the how-to. Financial attitudes and financial behaviors, however, are the implicit part of financial parenting that are mostly done on autopilot or ignored. If, for instance, children see parents fighting about money, this can give a very implicit connotation of ‘money = conflict’.

For a child to really grow up financially capable and financially self-reliant, they need the knowledge, they need the skills, and they need to make sure their money attitudes are not negative or associated with trauma. Critically, they need the skills to translate into behavior. How does knowledge become a habit or behavior that they are capable of? The missing element in most of the conversations around financial literacy, especially when we think of girls and women, is financial confidence.

Analysis by Cambridge University underpins this theory as money attitudes are largely shaped by age seven, and confidence is shaped by age five. The translation from knowledge and skills into behaviors is impacted by attitudes, but confidence is the key ingredient to make it all work. It’s what makes us comfortable putting a price tag on our work and investing in new areas.

Raising financially resilient children requires intentional modelling, early education, and open conversations about money.

Raising financially resilient children requires intentional modelling, early education, and open conversations about money. Parents should focus on making earning, saving, and responsible spending visible and meaningful, so that children develop lifelong financial capability and confidence. Critically, parents must focus on building a resources-first mindset in their children, as teaching them to earn before they spend sets them up for life. For wealthy families, this means preserving your legacy as well as your capital.

Professor of Family Business and Entrepreneurship at IMD

Peter Vogel is Professor of Family Business and Entrepreneurship, Director of the Global Family Business Center (GFBC), and Debiopharm Chair for Family Philanthropy at IMD, where he leads the Leading the Family Business, Leading the Family Office, and Lean Intrapreneurship programs. He is recognized globally as one of the foremost family business educators, advisors, and academics, and has received numerous awards and distinctions. He is the author of the award-winning books Family Philanthropy Navigator and Family Office Navigator.

Founder and CEO of SmartWayToStart

Mara Harvey is an IMD and Harvard-trained economist, senior finance leader, and pioneering voice in financial parenting. As Founder and CEO of SmartWayToStart, she equips parents and children with the financial literacy skills needed for lifelong resilience. With over 25 years in wealth management supporting billionaire families across Europe, she has led major social and digital innovation initiatives in the financial sector.

March 18, 2026 • by Ismaël Otsmani in Finance

European households hold trillions in bank deposits while participation in capital markets remains underdeveloped. Sweden offers an alternative approach. ...

March 9, 2026 in Finance

CFO Raphael Savalle explores how finance leaders can unite sustainability, AI, and human leadership to drive strategy in a fast-changing world....

February 24, 2026 in Finance

Schindler CFO Carla De Geyseleer explains how today’s CFO acts as a strategic co-pilot, uses sustainability to drive growth, and develops future finance leaders....

February 11, 2026 • by Catherine Agamis, Hischam El-Agamy in Finance

How banks can position themselves across multiple futures to deliver on sustainability commitments while maintaining financial performance...

Explore first person business intelligence from top minds curated for a global executive audience