IMD business school for management and leadership courses

Four Books That Show the Companies Firing Fastest Will Die First

It was early morning on March 28, 2007. In a Richmond-area Circuit City, the store manager stood in front of his staff at 8:15 a.m., staring at a script in his hands. Eleven long-tenured employees sat stone-faced. “You are terminated, effective immediately,” the manager read, voice steady and emotionless. Security personnel escorted them to the parking lot.

Across the country, 3,400 of Circuit City’s most experienced, highest-paid sales associates received the same news at the same hour. They had done everything the company asked. Many had gone to training and earned promotions for two decades. Now they were ushered out, given severance paperwork, and invited to reapply for their old jobs at a much lower wage.

The press release called it a “wage management initiative.” Anyone earning more than $18 an hour, roughly $37,000 a year, was gone.

Among those fired was Bobby Young, a twenty-year veteran. The next morning he appeared on Good Morning America, hurt and angry. “He wished me well, and that was it for twenty years of service,” Young said. “I have a family… I can’t live off $8 or $9 an hour.”

Circuit City CEO Philip Schoonover’s total compensation that year: $8.52 million.

Wall Street cheered. The stock rose 35 cents, or 1.9 percent, to close at $19.23. The spreadsheet showed immediate cost containment.

Then reality arrived. Within weeks the damage was unmistakable. April sales plunged. Customers walked into showrooms and found nobody who could explain how a home theater system worked. Analyst Tim Allen told the Washington Post the cause was obvious: experienced staff had been replaced with people who didn’t know the products.

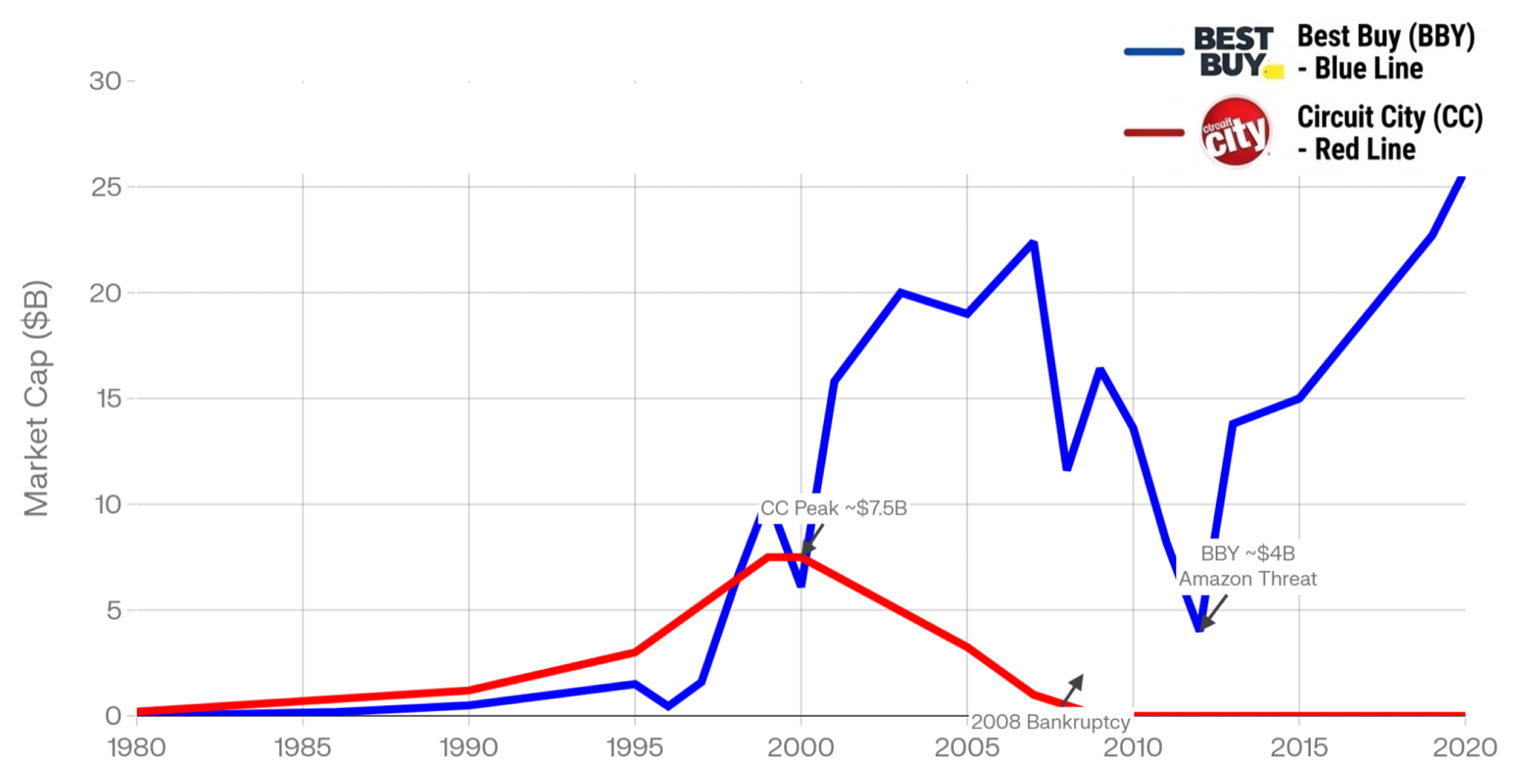

That holiday, same-store sales fell almost twelve percent. By year-end 2007, the stock price had collapsed to about $4.20, roughly a quarter of its March value. Less than two years after the mass firing, on November 10, 2008, Circuit City filed for Chapter 11 bankruptcy.

Circuit City had once been a pioneer. In the 1980s, it was the NYSE’s top-performing stock, a leader of the “big-box” electronics revolution. Jim Collins featured it in Good to Great. It had, within its own walls, all the information it needed to change course.

Yet at every juncture, leadership chose not to hear it. Instead, the company made endless tweaks. Training programs cut. Commissions slashed. Home appliances abruptly discontinued, all without pilots or data to test the impact. With each move, loyal customers and capable employees got pushed away.

Meanwhile, Best Buy kept reinventing.

In 1997, the two companies had similar revenues. By 2006, Best Buy had eclipsed Circuit City by more than 2.5 times in both sales and profit per employee, prospering even when Amazon’s shadow grew longer every year.

How did Circuit City lose its mind?

The Magic Bullet Mirage of 2026

That question is not historical. In the first quarter of 2026 alone, technology companies announced more than 45,000 layoffs. That’s a fifty-one percent increase from the prior year. The executives standing at podiums and typing shareholder letters are not citing financial distress or macroeconomic headwinds. They are citing artificial intelligence.

At Block, the digital payments company, CEO Jack Dorsey announced the elimination of 4,000 jobs, nearly half the workforce. He argued that the intelligence tools the company was building enabled smaller, flatter teams and fundamentally changed what it meant to run a company. Wall Street celebrated. The stock surged more than twenty percent.

Salesforce also slashed its customer support workforce. CEO Marc Benioff claimed that AI agents now handled half of all customer interactions. “I’ve reduced it from 9,000 heads to about 5,000 because I need less heads.” At WiseTech Global, the logistics software developer, the company cut 2,000 jobs, about 29 percent of its workforce. Chief executive Zubin Appoo said, “the era of manually writing code as the core act of engineering is over.”

Some of these decisions may prove disciplined. Some may turn out to be real surgery, the kind that removes drag without damaging the organ. But that is not what makes moments like this dangerous. What makes them dangerous is the speed with which one company’s announcement becomes another company’s permission slip.

Some will become cautionary tales, the kind that ends with rehiring the very people who were just ushered out. Consider X, where Elon Musk fired roughly eighty percent of his workforce, only to scramble and rehire when the servers went dark. Today, X’s user base has not grown. Its super-app ambitions remain unrealized. Not even close. Revenue fell from five billion dollars to roughly half that.

But most companies don’t have the deep pockets of an Elon Musk, or a venture community willing to keep propping up a damaged operation while they figure it out. Most have one shot to survive a structural transition.

So I want to know: when everyone is wielding the same axe, can anyone tell in advance who is performing surgery and who is simply hacking away? Who is exercising judgment and who is just copying the moves of others, unthinkingly?

If you were fired today and replaced by an AI “agent,” what is the one nuanced, human “workaround” or piece of tribal knowledge that the AI would never know to do?

That is your true value.

Because I fear that in 2026 we are witnessing the exact same pathology that destroyed Circuit City, playing out on a global scale, dressed in the language of artificial intelligence. Organizations do not die from a single bad bet. They die because the internal apparatus for perceiving reality, processing information, and executing strategy has already degraded.

I went looking for the answer where it would be hardest to hide: four books written by or about the CEOs at the center of these collapses. What they describe is the anatomy of a disease. It has a structure. And it begins, almost always, with what the organization can no longer see.

When Information Becomes Fiction

For most of the 1990s, nobody at Circuit City knew how the stores were actually performing. Not the regional vice presidents. Not the senior management team. Not even the board of directors.

In 1990, CEO Rick Sharp, who had built the company’s point-of-sale systems from scratch, launched an in-house credit card bank called First North American National. Within three years, hundreds of thousands of customers carried Circuit City plastic, and the credit-card operation was printing money.

But Sharp made a decision that would prove catastrophic: he folded the bank’s profits into the stores’ operating results. No separate line item. No disclosure. The bank’s earnings were applied to reduce general operating expenses, which made the store operations look far more profitable than they actually were.

That is how Best Buy was eating Circuit City’s lunch on volume and inventory turns, and nobody inside the company could see it. They looked at the consolidated bottom line and saw profit growth. They thought their model was superior.

“Middle management thought the stores were doing much better than Best Buy,” wrote Alan Wurtzel, the former CEO whose father had founded the company, “when in fact, without the bank, they were doing no better or worse.” The company, he concluded, was “fooling itself.”

Twelve hundred miles south, the same disease was eating through Blockbuster.

By the mid-1990s, Blockbuster had accumulated more data on the movie-viewing habits of Americans than any company in history. Every rental, every customer’s age, address, gender. Hundreds of millions of transactions. Its CEOs loved to boast about this massive database. But boasting was the only thing they ever did with it.

Catalog movies — the Drama, Comedy, Action, and Horror sections that filled at least half of every store — were essentially untracked. Blockbuster had no way to see how often those movies were rented.

Alan Payne, a longtime Blockbuster franchisee who had spent fifteen years at H-E-B (one of America’s best grocery retailers) was stunned when he discovered it. “If you asked that question of ten different Blockbuster executives,” he wrote, “you would get ten different answers. I did just that… and still, they did not know and did not care.”

You can’t fix what you cannot see.

So when Blockbuster finally launched its answer to Netflix in May 2004, an in-store subscription called the Movie Pass, it was flying blind. Pay a monthly fee, keep two or three DVDs out at a time, no late fees. Subscribers flooded in and grabbed mostly new releases, draining copies from the shelves and leaving regular customers empty-handed.

Franchisees begged headquarters for data. What titles were Movie Pass members renting? How many loyal customers were trading down from higher spending to a cheaper monthly subscription?

Blockbuster’s formal answer arrived in writing. “Currently the POS [store computer system] does not break down this information for reporting purposes.”

Meanwhile, Netflix built an algorithm called Cinematch that tracked what DVDs customers rented, what they saved to watch later, and what they skipped. The system then steered subscribers toward older movies that cost Netflix almost nothing.

Netflix was learning from every click. Blockbuster was guessing in fluorescent light.

Circuit City and Blockbuster. Same fatal gap. The apparatus for seeing reality had rotted from the inside. Once information becomes fiction, every decision that follows is built on sand.

The Tyranny of the Quarter

When David Cote took over Honeywell in 2002, he thought he was inheriting a bruised industrial giant. A botched merger, some leadership churn, a failed sale to GE. But underneath, solid businesses. That was the pitch. The board had kept him away from the financials for four-and-a-half months. When he finally got access, the forecast collapsed twenty percent within weeks.

He called his four division heads. “What the hell was going on?”

The targets, they told him, had never been real. Finance had handed them down anyway. “Just get it done. Do whatever you need to make the numbers.”

Then Cote sat in on his first “make the quarter” meeting. Finance presented a list of actions required to hit the quarterly number. Cote scanned it. Not one item involved selling more product or reducing a real cost. Every action was a paper transaction: sell a business to book a one-time gain. Restructure a vendor contract to pull future revenue into the present. Change an accounting method to recognize income sooner.

But nothing in the conference rooms prepared Cote for Louisiana.

He paid an unannounced visit to a Honeywell chemical plant. The manager walked him through operations, then outside. Cote looked out across vast, flat, treeless fields stretching to the horizon.

“See those fields out there?” the manager asked. “Those all used to be trees.”

One quarter, to make his numbers, the manager had the entire stand cut down and sold for timber. He spent most of the quarter managing the logging transaction instead of running the plant. When the sale closed, he made his target. He even received a corporate award for creativity. Headquarters was so impressed it began checking whether other plants also had forests to cut down.

The same short-term logic also applied in Circuit City’s C-suite. Between 2003 and 2007, the board authorized four separate stock buyback programs, spending $920 million to repurchase shares at an average price just north of twenty dollars. The architect was CEO Alan McCollough, whom Wurtzel described as always anxious to please Wall Street.

Meanwhile, same-store sales had not improved since 2000. In the five years after the first buyback, the company earned a total of $190 million on fifty-four billion in revenue, a margin of less than half a percent. By year-end 2007, the stock sat at $4.20. The billion dollars spent on buybacks was gone. Cash that could have funded store renovations, new technology, or the people who once made the whole thing work.

That Louisiana plant manager didn’t set out to cut down a forest. He’d simply been trained, quarter by quarter, to treat everything around him as fuel for the next quarterly number. You don’t need to run a chemical plant to recognize the pattern.

What number are you hitting right now that you know doesn’t reflect what’s actually meaningful?

In both companies, the tyranny worked the same way. The pressure to deliver this quarter’s numbers first distorted the data, then the decisions, then the organization’s ability to see what was happening on the sales floor or factory line.

When Leaders Stop Thinking

Once the first two steps happen, a peculiar form of paralysis sets in. It isn’t that the leaders are inactive. It’s that they’ve stopped doing the one thing they are paid for: thinking.

For years, Alan Payne, Blockbuster’s most profitable franchisee, had sent detailed memos to CEO John Antioco and his senior team showing that the stores were failing at basic inventory management. When he presented the data in meetings, he got polite disagreement. When he followed up in writing, the replies came back in “corporate-speak.” When he pointed out that eighty million American households now owned DVD players and no longer wanted VHS tapes, headquarters had a phrase ready. “The customer is format agnostic.”

Eventually Payne stopped trying. “It was a waste of my time.”

Then came the latest “big idea” announcement in December 2004. Eliminate late fees. The franchisees had already voted no. Their stores lived and died on a simple rule: Movies had to come back on time. Without that, the shelves emptied and the economics collapsed.

What are people thinking? A studio executive who played golf with Antioco in 2002 said the CEO’s favorite subject was his ranch. Not Blockbuster. Not the business. His pattern had become its own kind of management: weeks of disengagement, then a celebrity appearance to fire up the troops, then gone. The people closest to Antioco were blunter. “If you want to rule the world, you’ve got to show up. John did not show up.”

Nine hundred miles north, Circuit City was drifting toward the same surrender. Ann-Marie Stephens had built something that was actually working. In Colonial Heights, her secret prototype store was based on fresh research into why women and teenagers disliked Circuit City and why Best Buy kept pulling away. The design changed the floor plan, softened the sales model, and made browsing easier.

The store took off. Sales ran 27 percent above the nearby Petersburg location it replaced, and customer feedback, especially from women, improved markedly. Stephens wanted to test, refine, and learn. Instead, management stripped out key elements and rolled a diluted version across Chicago. Sales didn’t improve.

Then one morning, Stephens was in Florida scouting locations for a new appliance store when her phone rang. Come back to Richmond. The decision had been made to exit appliances entirely. Over a billion dollars in revenue, gone.

Complex questions about talent, customer experience, and Best Buy’s encroachment were reduced to spreadsheets and analyst optics. The 2007 “wage management initiative” followed the same logic. Fire 3,400 veterans at 8:15 a.m. across the country. No pilots, no field tests, just math on paper.

Alan Payne sent the memos. Ann-Marie Stephens built the prototype. Both had the data. Both stopped trying, because they weren’t being heard.

Who on your team has stopped telling the truth, and what happened the last time they tried?

Their silence is not neutral.

The disease had entered its final phase. First, the information had become fiction. Then the quarter ate the future. Now the people at the top had stopped thinking altogether — not because anyone was stupid, but because the system had made not-thinking the path of least resistance.

The Blue Shirt Test

Hubert Joly took over Best Buy in September 2012, when the company was in the same death spiral. Bloomberg Businessweek had just put a zombie in a blue shirt on its cover. Everyone expected the same playbook: slash headcount, close stores, strip the carcass for parts.

Instead, on his first day as CEO, Joly drove sixty miles to a Best Buy in St. Cloud, Minnesota. He put on a blue shirt with a “CEO in Training” tag and spent three days listening to frontline employees. What he learned in those seventy-two hours he could never have learned from spreadsheets at headquarters. A broken website search engine. Floor plans that gave prime real estate to dying product categories. Demoralized staff who had just seen their employee discount gutted.

The turnaround that followed was, in his words, “the antithesis of the blood sport… the opposite of ‘cut, cut, cut.’” Best Buy’s stock went from $11 to over $100. The company is still standing.

Here is the test for 2026: When a company announces that AI has made thousands of your colleagues redundant, ask one question. Did anyone go to the floor first? Did anyone put on the blue shirt, sit with the people doing the work, and learn what would actually break?

This is what I know. When the technology disappoints, when the promised efficiencies don’t materialize, when customer loyalty evaporates, and when there is no one left on the floor who actually understands the business, Wall Street will not save those companies. Organizations die from AI disruption because their leaders already lost their minds, forgetting that business has always been, and will always be, a fundamentally human enterprise.

The winners will not be the firms that fire fastest. They will be the ones that can still think, still listen, still see. The rest will call it transformation all the way down.

Then one day, the lights will go out.