IMD business school for management and leadership courses

Why the world’s most valuable companies are suddenly buying nuclear plants, pouring concrete, and owning the whole stack.

The most valuable companies in the world just reversed the one rule that made them valuable. For a decade, the smartest move in business was to own as little as possible.

The mantra was “asset-light”: Outsource your factories like how Apple handed manufacturing to Foxconn, rent your infrastructure the way that everyone rents AWS, and keep the brand and the software while shedding the concrete and the steel.

That was the gospel. It was why people said Airbnb was beating Hilton without owning a single hotel and why Uber was killing the taxi business without owning a single car.

The market just tore up the gospel.

Look at the capital expenditures of the Magnificent Seven over the last 18 months. Almost since the internet arrived, we have never seen top technology companies spend so much on physical infrastructure.

Capital Expenditures/Total Assets (Last Twelve Months)

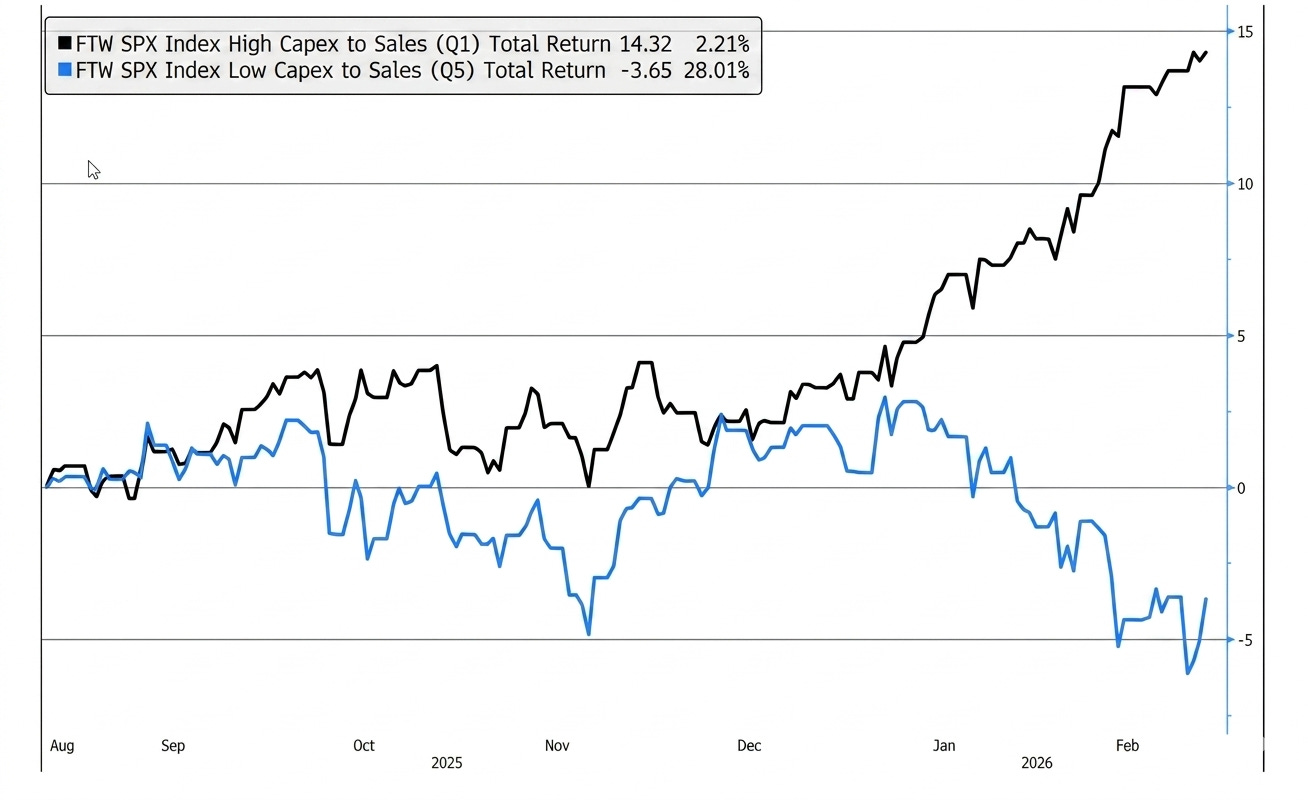

The market is now aggressively rewarding asset-heavy companies with high capital expense-to-sales ratios while heavily penalizing asset-light indices.

Performance of US Asset Heavy (High Capital Expense to Sales ratio) to Asset Light FTW SPX Stock Indices – Past 6 Months, August 2025 to February 2026

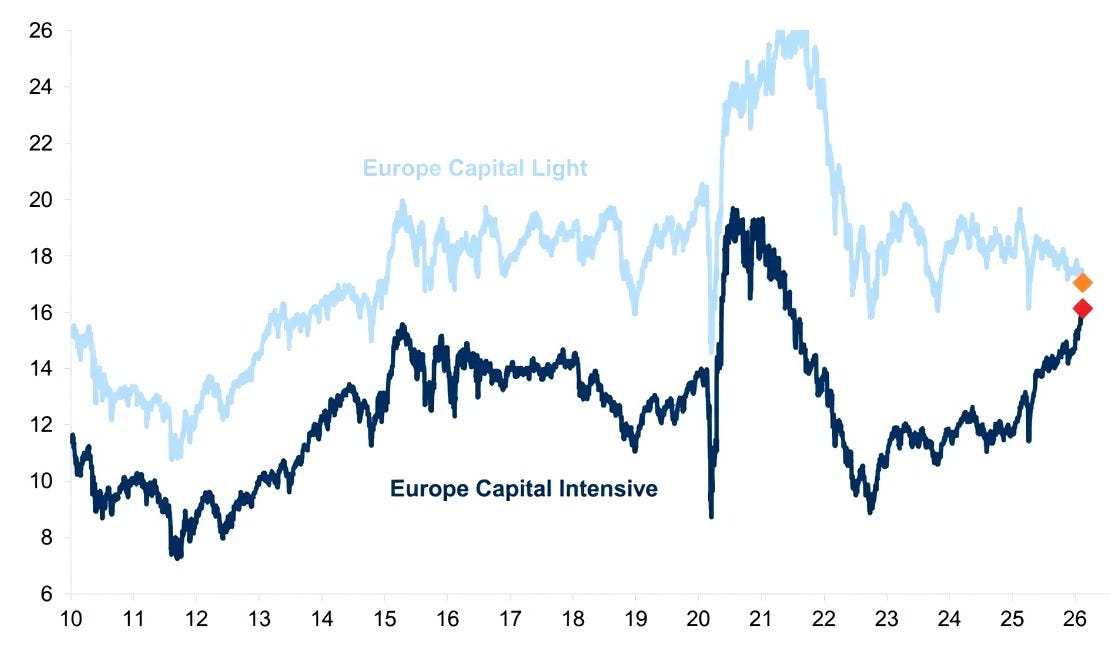

This is not just a Silicon Valley story. In fact, the same re-rating is hitting Europe. And the labels we have used to sort companies for a century no longer mean anything.

Capital Intensive valuations have re-rated, 12-month fwd P/E

Think about what these firms are doing. The world’s leading credit card company announced that it would pay up to $1.8 billion for a stablecoin operation, allowing it to move money on crypto rails. A software giant signed a 20-year contract to restart a nuclear reactor. A carmaker became one of the world’s largest builders of stationary battery storage. And a phone maker launched an electric car that was faster than a Porsche and cheaper than a Tesla Model S.

When I look at these examples, I want to know one thing: Who is building a durable advantage, and who is just burning cash out of panic? We need a new scoreboard to separate the genuine frontrunners from the laggards.

To answer that, we ran the data through the IMD Future Readiness Indicator, released last week.

Whether you’re a CEO trying to redesign your operating model before your competitors do, a middle manager deciding which cross-functional projects to aggressively champion, an individual contributor evaluating if your current company is a sinking ship, or an investor trying to spot the next massive wealth reallocation, one thing is certain: You cannot afford to look away.

The companies winning in 2026 are doing the one thing that every business-school case study told them not to do.

They are reintegrating.

The reintegration of the automobile

In 2011, a Bloomberg TV host asked Elon Musk whether China’s BYD might challenge Tesla one day. Musk threw his head back and laughed. “Have you seen their car?” he asked. At the time, it was a fair point. Why worry about an obscure battery maker churning out utilitarian taxis?

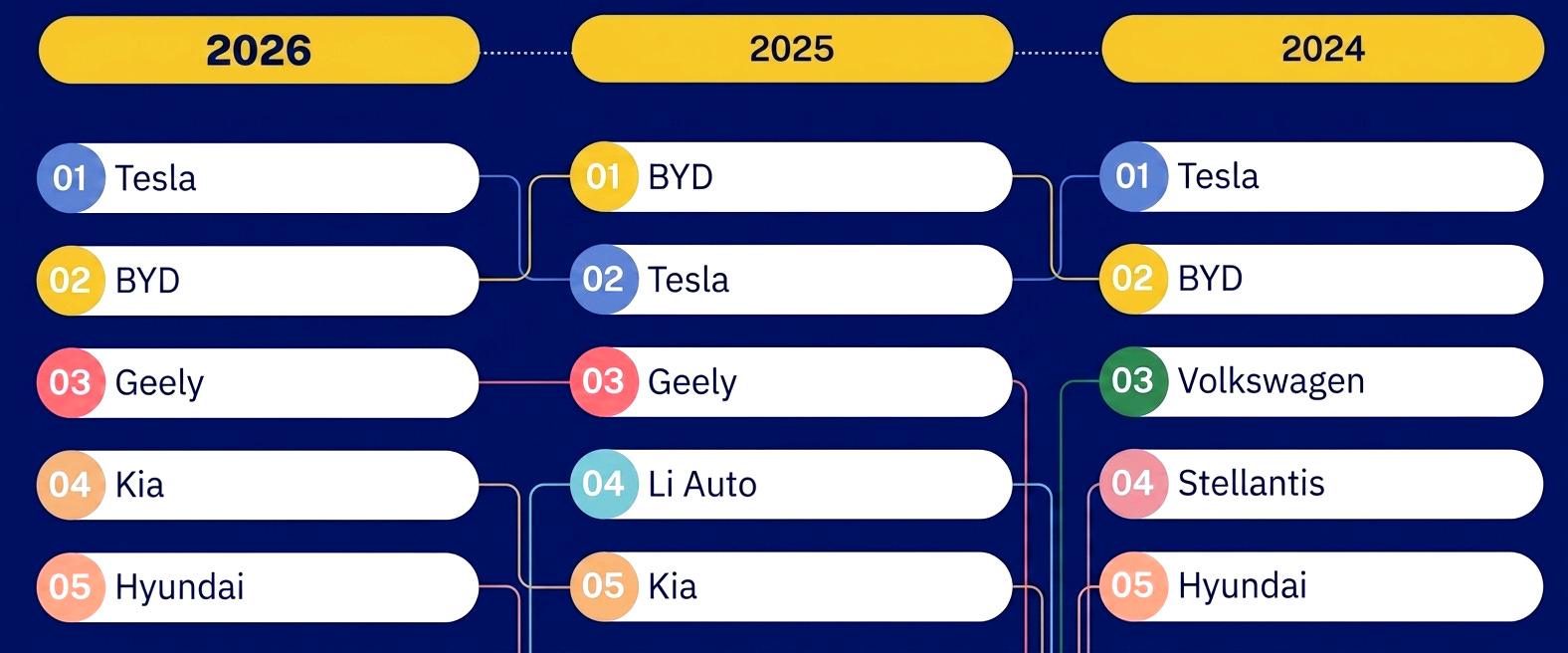

By the close of 2025, BYD had taken the global crown for all-electric vehicles, outselling Tesla by more than 600,000 cars.

When my team fed the 2026 data into the indicator, the auto leaderboard had been rewritten. In 2024, the top five included a familiar mix of legacy—BYD, Volkswagen, Stellantis, Hyundai—plus Tesla. By 2026, the companies were Tesla, BYD, Geely, Kia, and Hyundai. The center of gravity has moved to Asia, and the Western giants are sliding out of the top tier as they struggle with software and battery integration.

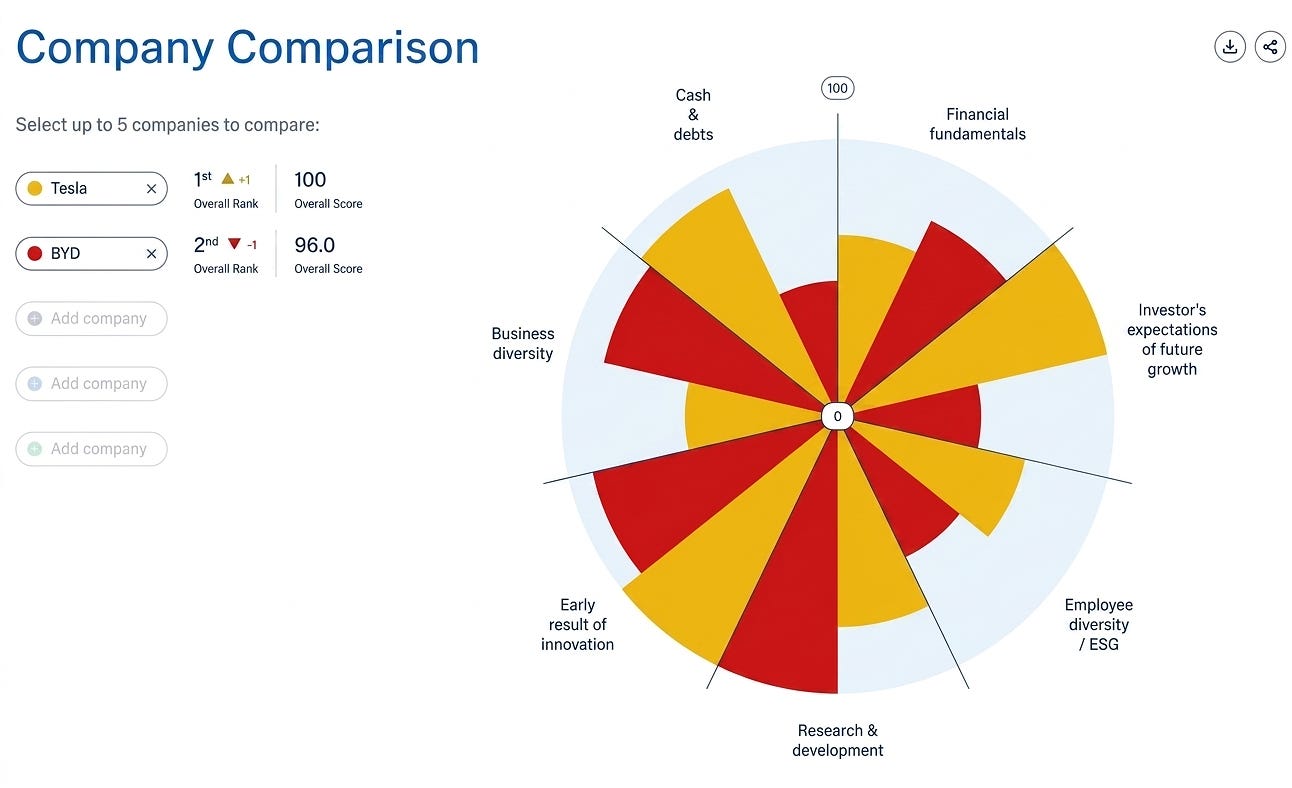

Tesla still ranked first overall, with a perfect 100 on Investor Expectations and Innovation Results. However, its shape was unusual. The market wasn’t paying for the cars. Instead, it was paying for the rest. Tens of thousands of GPUs humming in the Cortex facility in Texas. A record 46.7 gigawatt-hours of battery storage deployed in a single year. Take away the Full Self-Driving software and the energy grid, and what remains is just a normal car company.

Now look at BYD: an operations-driven machine that scored a perfect 100 on R&D. CEO Wang Chuanfu never cared about investor hype. He cared about physics. He remembered what happened in 2012, when a drunk driver doing 180 km/h slammed into a BYD taxi in Shenzhen. The car hit a tree and caught fire, and three people died.

How do you make a fire like that physically impossible? You control every layer, from the cathode in the lithium iron phosphate Blade Battery to the silicon carbide chips that switch the current. You build an industrial park in Shenshan four and a half times the size of Tesla’s Shanghai plant. You cast your own motors. You print your own boards. And because you own the whole stack, you can mass-produce an SUV that floats across floodwater and a hypercar that hits 496 km/h, the fastest speed that a production car has ever been driven.

The asset-light playbook (buy standard parts, focus on brand, let someone else make the hard stuff) was the right answer for the 2010s. But it was the wrong answer for 2026. The carmakers who built the stack won, while the carmakers who rented it are dropping out.

How we built the scoreboard

If old labels are useless and if last quarter’s margin can’t tell you who survives, you need a different way to measure. So we built one.

The IMD Future Readiness Indicator looks past quarterly profit to capture how well a company is scaling new capabilities. We track 45 hard-data variables across seven equally weighted pillars: financial fundamentals, investor expectations, business diversity, ESG, R&D, early results of innovation, and cash.

And we don’t trust self-reported surveys. We scrape the evidence: patent filings from Espacenet, venture flows from Crunchbase, sustainability ratings from Sustainalytics, and a structured rubric that scores early innovation across product, software, autonomy, and manufacturing instead of counting press releases.

Future readiness is never a single bet. You can’t just be a hardware company, and you can’t just be a software company. To build a durable advantage today, you have to stack the capabilities, silicon, code, power, and manufacturing. Then you have to control how those layers fit together. Single-layer plays get arbitraged away almost overnight.

When money becomes software

Finance looks nothing like automotive. That’s why the same pattern is so revealing when it appears in both industries.

For 50 years, the rules of global finance were simple. Every credit card account had a human behind it. Every cross-border payment ran on SWIFT, the dollar-clearing network that has dominated the world since the 1970s.

Both rules just broke.

By the spring of 2026, China’s Cross‑Border Interbank Payment System was handling that kind of flow as a matter of routine. In March alone, its average daily transaction value climbed to about 920 billion yuan, almost 50 percent higher than February. CIPS now connects roughly 4,900 banks across 187 countries. SWIFT is still bigger overall, but it’s no longer the unassailable monopoly.

Then on July 18, 2025, President Trump signed the GENIUS Act into law, giving dollar-pegged stablecoins their first federal rulebook in the United States. Total stablecoin transaction volume that year hit $33 trillion. Tether’s market capitalization reached $187 billion.

The buyers changed, too. We are no longer just dealing with humans tapping plastic at a coffee shop. AI agents now compare and buy products, issue cryptographic credentials, authenticate at checkout, and are handed spending authority by banks.

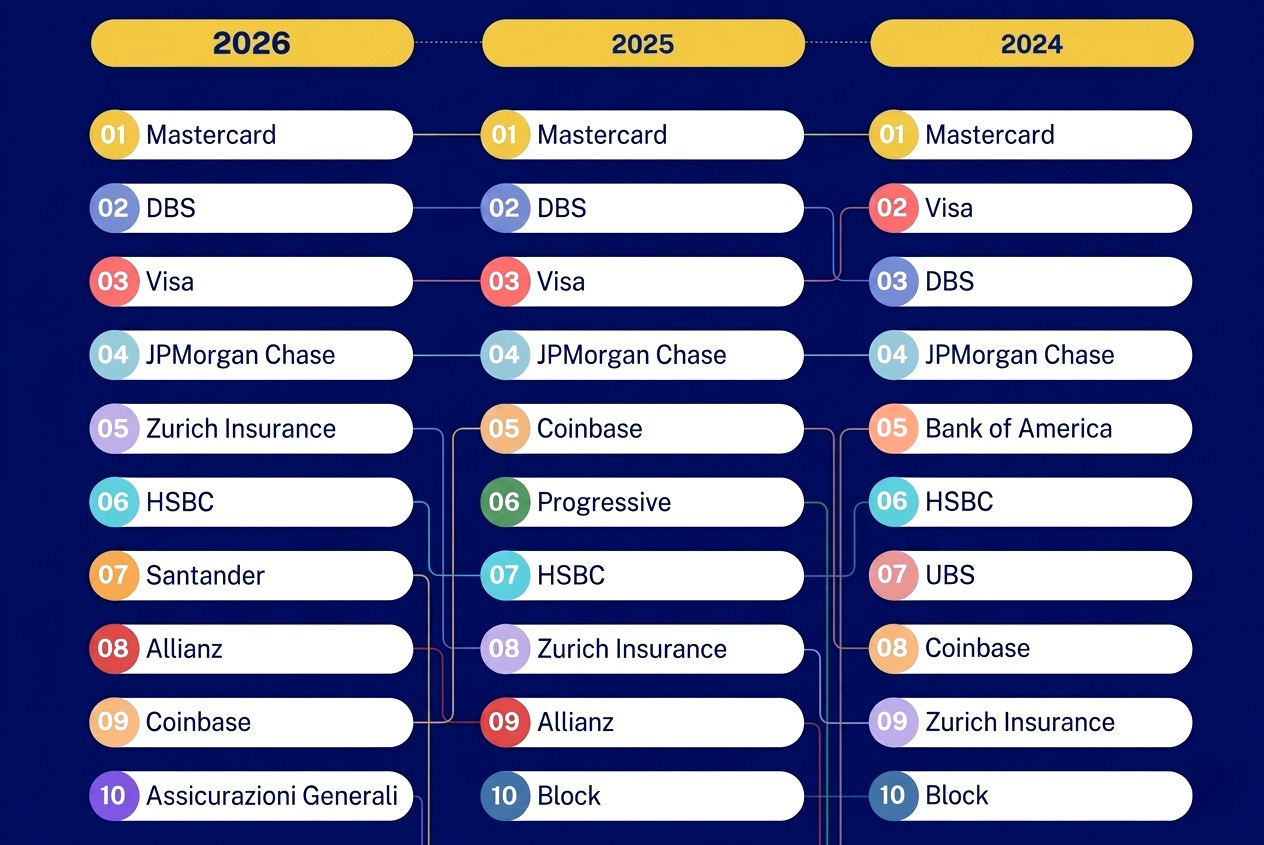

When the barriers protecting banks and networks dissolve, how do you tell who survives? We ran 39 financial institutions through the 2026 indicator, and the result mirrored the shock in autos. The winners are the ones reintegrating their stacks to own the new rails of commerce.

Look at Mastercard. CEO Michael Miebach understood that a single monolithic network wouldn’t survive a fragmented digital future. That’s why Mastercard is branching into everything. In April 2025, it launched Agent Pay, which lets an AI agent transact on your behalf. Five months later, OpenAI launched its own Instant Checkout on a rival stack built by Stripe. Visa and Google rushed out their own versions. Overnight, the race to own the agentic checkout became the only race that mattered.

Then, because the old card network is no longer enough, Mastercard agreed to pay up to $1.8 billion for BVNK, a stablecoin infrastructure firm, to own digital settlement end to end. Stablecoin acceptance is no longer a fringe crypto experiment. It’s a treasury question. SpaceX already collects Starlink revenue through stablecoins in markets where local banking is unreliable. Mastercard is not trying to remain a credit card company. Instead, it’s trying to become the operating system of the programmable, agentic economy.

DBS tells the same story from inside a bank. In March 2025, Tan Su Shan became CEO. Despite being warned by her board that even the chief executive’s job could one day be replaced by AI, she did not wait to be disrupted. By the end of 2025, DBS had deployed over 2,000 AI models in live production, generating roughly S$1 billion in pure economic value for the bank.

Both companies figured out the same thing: A regulated reputation is the most valuable asset they have. Combine trust, data, identity, AI, and programmable settlement, then you can move into territory that once belonged to fintechs. Do not rent the new rails. Own them.

When good enough suddenly isn’t

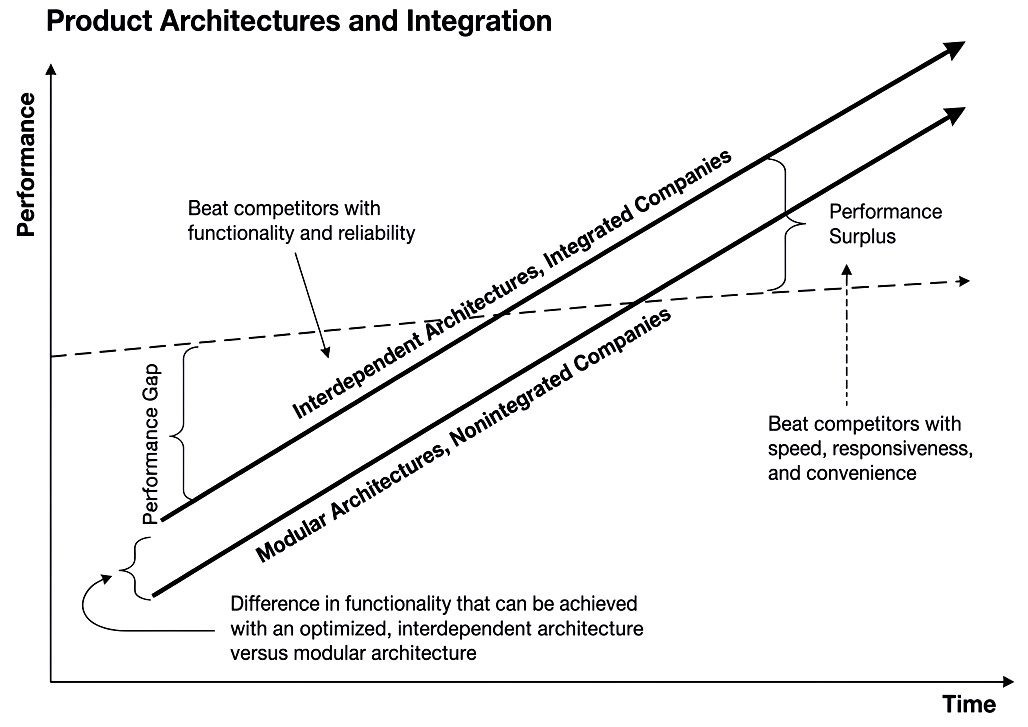

Why are a battery maker and a payment network suddenly running the same playbook? The answer is an old one. The late Harvard professor Clayton Christensen worked it out decades ago by studying the constant tug-of-war between modularity and integration.

I sat in his doctoral seminar two decades ago, and I remember that he kept drawing the same diagram on the whiteboard. A pair of rising lines. One steep, one shallow. The steep line was customer demand. The shallow line was what modular components could deliver. As long as customer demand outpaced modular performance, the integrated firm won. It could squeeze every drop of performance from a proprietary architecture. Own the design. Own the hardware. Own the software. That was IBM mainframes in the 1960s.

Eventually, the technology overshoots what customers actually need. The customer stops caring about raw power in favor of price and convenience. The industry fractures into modular pieces. Best-of-breed suppliers win. That was the PC industry in the 1990s, with HP, Dell, Compaq, and IBM’s ThinkPad all assembling third-party components into commodity boxes.

But Christensen warned of a trap. Sometimes the frontier shifts so violently that the old modular pieces stop fitting. When that happens, the product is suddenly not good enough again. This is exactly what just happened to cars and finance.

For three decades, automakers outsourced almost everything: standard brakes, standard software, and standard batteries. The electric vehicle broke that. Off-the-shelf cells and code could not deliver the range, safety, and compute that buyers wanted, so Tesla and BYD abandoned modularity and integrated the whole stack, from the battery cathode to the silicon.

The same shift hit finance. For half a century, the four-party card network was more than good enough. You swipe, a bank clears it, and a merchant gets paid. But when AI agents fire off rapid purchases and when stablecoins bypass the old plumbing, the old system breaks. Mastercard and DBS reintegrated to own the new programmable rails.

What to do on Monday morning

I keep getting one question after I present this data: “Howard, does this apply to my industry?”

Nobody can tell you that from the outside. But you can tell yourself. Here are three questions for Monday:

- What are your customers actually complaining about? If it’s raw performance or reliability, you’re not good enough yet, and you need to integrate. If it’s price or convenience, you’ve overshot, and you need to modularize.

- Look at your supply chain. Are you outsourcing because the outside supplier is actually better, or are you outsourcing because it was the default answer in the 2010s and nobody bothered to question it?

- Finally, take the hardest, most intractable problem that your company has to solve next year. Who actually owns the physical and digital layers required to solve it? Do you control them? Or are you entirely at the mercy of one vendor?

If your answer to the last question is the vendor, you do not own your future. You are renting it.

Why software is a commodity and power is king

The room is always cold. It’s what you notice before you notice the servers, the white floor, the rows of cabinets, or the whirl of cooling fans loud enough to drown out conversation. A hyperscale data center does not look like a factory, but it is.

The new heavy industry is cognition. It turns electricity into intelligence.

For the past year, the press obsessed over which tech giant had the smartest frontier model. The leaders themselves realized that something else was the bottleneck.

On January 12, 2026, Apple signed a deal to run Apple Intelligence on a custom Gemini model from Google. They reportedly pay around $1 billion a year, plug it in, and call it Siri. The intelligence is now modular, a swappable part.

What you can’t swap is physics. By 2030, on the high end of EPRI’s projections, data centers could draw as much as 17% of all U.S. electricity, up from roughly 4% today. When the wind dies and the sun sets over Loudoun County, Virginia, a gigawatt data center still has to pull the power of a small steel mill. That’s not something you can solve in software. You have to integrate the energy stack.

That’s why the leaders in our ranking are doing things that sound absurd for tech companies. They are becoming electric utilities.

The date is September 20, 2024. Joe Dominguez, CEO of Constellation Energy, signs a contract for 835 megawatts of around-the-clock power. The buyer is Microsoft. The plant is Three Mile Island, the same site that melted half a reactor core in 1979 and became a permanent synonym for disaster. Microsoft committed to buy every watt from the restarted Unit 1 for twenty years.

They are not alone. Amazon contracted for more than 5 gigawatts planned capacity of pebble-bed reactors from a Maryland startup. Google signed a master with Kairos Power to seed its data centers with small modular reactors that use molten salt as coolant and pebble fuel—advanced nuclear wired straight into the AI stack. Meta announced three separate nuclear deals in a single day, locking up as much as 6.6 gigawatts to feed Prometheus, its enormous AI campus rising out of the Ohio farmland.

The companies at the top have realized that the hard problem is no longer compute. Silicon keeps getting faster. Algorithms keep getting leaner. But a data center cannot think without power. The smartphone era was about elegance and design. However, the AI supercycle is about who controls the silicon, the power contracts, and the cooling water.

The Physics of Innovation

Look at your corporate calendar for next week. Somewhere on it is a meeting about a vendor contract, a cloud subscription, or a partnership. For a decade, we sat in meetings exactly like that, telling each other that the smart move was to rent the infrastructure and focus on the brand. We were sure that the asset-light model was the only sensible way to run a business.

But it wasn’t.

The companies pulling ahead in our 2026 data are the ones tearing up those contracts. They are pouring concrete, restarting reactors, and casting their own silicon. They understood that when the technology shifts this hard, the standard off-the-shelf pieces simply stop working. Christensen told us that to survive a major technological transition, you cannot run on someone else’s standardized parts.

And that’s why in 2026, integrated companies keep winning when the world fragments.