We see that a big change in Net Sentiment Scores (NSS™) from before the March 19 events to the quarter following them concerns the SFC: from a fully positive score before the CS crisis, sentiment on the SFC has become marginally negative. The limited number of observations before the crisis suggests that SFC was not news to many. The sentiment has now turned, even if not necessarily negative, but suggesting vulnerability. Stakeholders have noted events contributing to a loss of positive sentiment toward the SFC. That by itself deserves tracking going forward.

The Swiss Government lost some points, the SNB gained some. These are not significant changes. However, what cannot be argued, is that the decisive intervention has helped the standing of the Swiss Government.

Sentiment on Swiss market authorities (FINMA) has turned negative. The Swiss National Bank has, albeit marginally, reduced the negative sentiment against it.

Based on these preliminary data, one can conclude that there is an issue around Swiss market authorities, which the Expert Group has indeed identified and started to address.

Work ahead for UBS

Turning now to the banks, not all banks were negatively affected by the CS crisis. Raiffeisen even gained favors over the period, while the sentiment on Julius Bear remained unchanged. Swiss banks, except for CS and UBS, have maintained their position or even improved theirs. They appear to have convinced their stakeholders that they were at a good and safe distance from the crisis and that CS and UBS were the main actors, with the Swiss authorities.

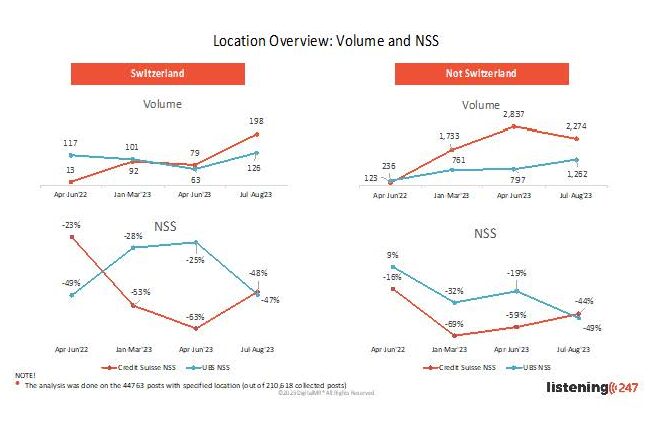

The examination of NSS™ dynamics of the two banks directly concerned by the CS takeover provides interesting conclusions.

Unfortunately, the sentiment of both Swiss and foreigners is a negative one. NSSÔ methodology identifies this as connoting a risk factor, and a vulnerability going forward.

Interestingly, the Swiss and foreigners have followed different paths to arrive at their shared negative sentiment. CS had negative ratings entering the crisis, in Switzerland and abroad, underlining its risky position. This sentiment became more pronounced during the crisis and then started to recover, albeit marginally, with its absorption into UBS.

The UBS story is a different one. It already had a negative NSS™ in Switzerland before the crisis. This sentiment initially became less negative – presumably due to its role in rescuing CS. The positive Swiss sentiment, however, disappeared six months after the event. UBS, in Switzerland, is now back where it was 12 months ago. This may be the result of its initial apparent reluctance to bail out CS, or its hard and dominant negotiating position. There is no “white knight” effect. If anything, the contrary.

Worrisome too is that the sentiment abroad has joined the Swiss sentiment, at considerably negative levels. The CS crisis has deteriorated UBS’s sentiment position abroad, with UBS fully absorbing the negative sentiment on CS.

Work ahead thus for UBS, which is now financially larger, but also riskier given the negative NSS™. As has been stated earlier, NSS™ is considered a good predictor of risk. The UBS CEO recently admitted to this through his pointed remarks against the Swiss cantonal banks. His remark that together these cantonal banks presented a greater systemic risk than UBS defies any logic. These banks are guaranteed by their cantons, they largely do not operate abroad, nor do they have big investment banking units. Most importantly, their risks are not concentrated and aggregated in any way. Second, the NSS™ analysis provides one explanation for the outflows of deposits towards these cantonal banks, which the CS takeover will not counter, nor will the CEO’s surprising statements. These comments run counter to recent comments by the Chairman of the SNB who is pleading with customers to be more mobile when considering competitive offers from banks.

The government’s intervention in CS

The review of the governance and management of the CS crisis by the various authorities triggers a few fundamental questions. What was the plan driving the intervention of the Swiss authorities? If there was a plan, why were more assertive interventions not triggered, and earlier, even with their limited hard powers? Interventions at board and governance levels (e.g., by prompting a change in the Chairman) can be rapid and swift; but all interventions appeared at best timid, if not absent altogether. How, for example, did the Swiss authorities allow the hiring by CS of a CEO from the insurance industry (a sector we consider related but distinct from banking), when the two senior-most leaders of the company were not banking experts either the Chairman was a lawyer, and the Vice Chairman was a full-time CEO of a pharmaceuticals company)? Why didn’t the authorities ask for changes to the CS business model and why didn’t they develop a toolkit for handling them?