IMD business school for management and leadership courses

How AI Agents and the Death of Normal Are Rewriting Organizations

In 1931, a twenty-year-old commerce student at the London School of Economics received a modest traveling scholarship and boarded a ship to the United States. His name was Ronald Coase. He had worn leg braces as a child. Economics had found him almost by accident, in a seminar where a professor unpacked Adam Smith’s theory of the invisible hand.

“It was a revelation,” Coase would remember decades later. He had planned to study law. Instead, armed with letters of introduction from a Bank of England contact, he spent a year visiting Ford plants, General Motors factories, and a long list of American businesses, puzzling over a question:

Why do firms exist?

The question came to him while watching how real industries organized themselves. Some activities stayed inside the company. Others were contracted out. So if markets are as efficient as Adam Smith suggested, why build firms at all? Why hierarchies? Why middle managers? Why conference rooms, reporting lines, and org charts?

Coase wrote up his answer in an essay published in November 1937, when he was twenty-six. He titled it “The Nature of the Firm.”

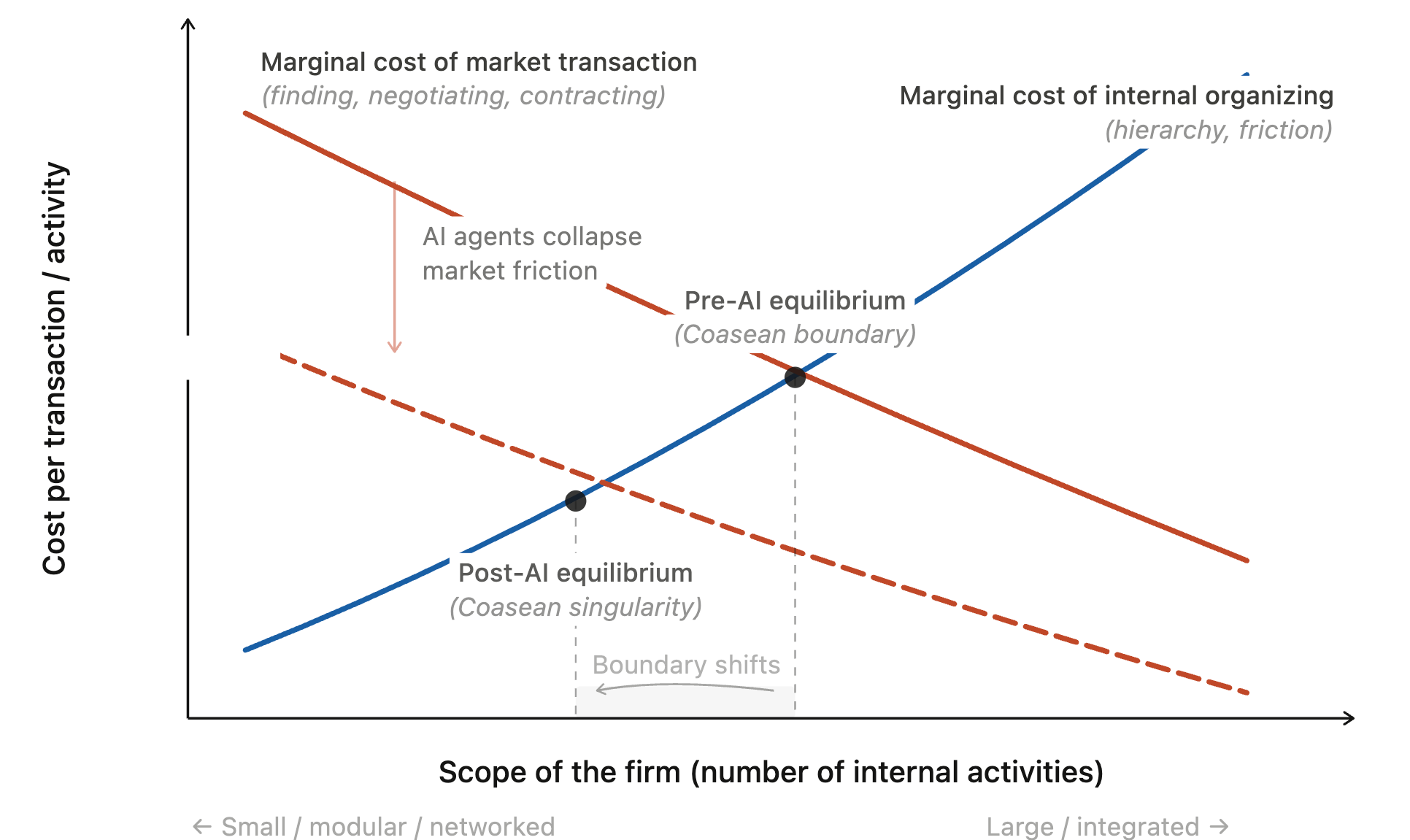

The idea was simple: Markets are expensive to use.

Friction is everywhere. Finding a spinner takes time. Negotiating the price for every yard of yarn takes effort. Writing a contract for every afternoon of work takes a lawyer. These are transaction costs. Many of them are replaced inside the firm by something blunter and cheaper: authority. A manager tells an employee what to do.

The firm expands until the cost of organizing one more transaction internally equals the cost of carrying it out through the market.

That is the boundary of the firm.

The essay was short. Dry, even. Coase published it in Economica. Fifty-four years later, in 1991, it helped earn him the Nobel Prize in economics.

For close to a century, the theory has held.

It explained why companies got big during the industrial age (coordination was expensive, so internalize everything), why they got flatter during the internet age (email and ERP systems reduced internal coordination costs), and why outsourcing boomed in the 2000s (India’s IT services made market transactions cheap enough to push work outside the firm).

Now, in 2026, Claude and other AI agents are pushing Coase’s logic toward its limit.

On the supply side, AI is collapsing coordination costs in ways the internet never could. An agent can draft a contract, source a supplier, negotiate terms, and monitor delivery. That persistent friction of the past is finally dissolving.

On the demand side, the comfortable middle of the market is thinning. The place where Applebee’s fed families, where Gap clothed the masses, and where standard software packages served nearly everyone has been hollowing out. What remains is a barbell: the ultra-cheap and algorithmic on one end, the hyper-personal and curated on the other.

AI did not create these forces. It is accelerating both at once. Driving coordination costs lower on the supply side. Splintering expectations further on the demand side. And the result is rewiring the firm and rewriting our jobs.

Firms will not disappear. Jobs will not disappear. But in a world moving toward near-zero transaction costs, both are being remade. This is what it looks like when Coase meets Claude.

I call this the Coasean Singularity.

The Death of Normal

In 2007, you walked into a theater and bought a ticket. No research. No TikTok. You picked a movie because it started at 7:30pm and your date liked George Clooney. That was enough.

Michael Clayton cost $21 million. It was nominated for Best Picture. It was a movie for adults, made by a studio, distributed widely. People who sold insurance watched it. People who taught high school watched it. People who were on their second date and just picked something watched it.

That movie does not get made today.

What replaced it is a barbell. One end is the $200 million superhero franchise. The other end is the $7 million A24 film about grief and mushrooms. The middle is gone. Those boutique masterpieces are smarter. They reach exactly those who already know what they’re looking for, thanks to Instagram and TikTok.

The middle of every major consumer market is collapsing. Films, restaurants, music, retail, careers. What is replacing it is a barbell. Enormous weight on each end. Nothing in the center.

Walk into a strip mall and you can see it. In May 2024, Red Lobster filed for bankruptcy under roughly $300 million of debt. James Berke, 23, a server in New Jersey, woke up Monday to the place padlocked. The parking lot was full and the doors were locked and nobody had said a word. “They made us work Mother’s Day to get that quick buck, and then they closed us.” Freezers were carted out. Booths auctioned off. Lobster tanks drained. More than 130 locations closed.

Red Lobster wasn’t alone. TGI Fridays shuttered 185 locations. Denny’s closed up to 150. Applebee’s trimmed 47. Hooters, Buca di Beppo, and dozens of restaurant chains filed for bankruptcy in 2025 alone.

But Sweetgreen’s shredded kale and wild rice bowl is doing fine. The taco truck is doing fine.

The premium survived. The cheap survived.

The place where a janitor and an accountant once sat in the same room and ordered from the same menu is what’s disappearing.

And no one seems to think that is a problem, which tells you exactly who the replacements were built for. They are more interesting; they serve fewer people.

The cultural monoculture vanished somewhere around the Game of Thrones finale in May 2019. That was the last time 19.3 million people watched the same thing on the same night. Nothing since has come close. Algorithmic feeds now create individual reality tunnels. TikTok spins new ones every few weeks. Shein adds six thousand new styles a day. Trends flash, peak, and vanish.

That’s how consumers stopped wanting “good enough for people like me.” They want good enough for me. You can see that inside your own company, too.

Microsoft and LinkedIn found that 75% of knowledge workers already use AI at work. And 78% of AI users are bringing their own tools, because the company-issued version feels generic. Bosses call this shadow IT and treat it as a compliance problem. But these were not rogue employees. They were the diligent ones. The ones who stayed late. They just wanted tools that worked the way they worked.

The market has ceased to be a mass. Demand is distributed, specific, shifting, and impatient.

People want software, clothes, meals, careers shaped to their exact workflow, their exact body, their exact mood.

Companies have taken notice. Pernod Ricard now tracks how AI models talk about its whisky brands and uses those insights to refine its marketing and creative. Instacart built a ChatGPT plugin that lets you add groceries to your shopping cart mid‑conversation, and has since made it a full in‑ChatGPT flow.

These are real adaptations. They are also mostly interface moves. They will not be enough. When you get AI to highlight Ballantine’s as affordable in real time, that does not help you launch a limited-edition single malt in seventy-two hours because a TikTok bartender in Seoul just made peat smoke go viral.

Serving those ephemeral demands requires a supply structure that can spin up fast, go narrow, and dissolve when the moment passes. Most firms still plan in annual cycles, manufacture in big batches, and launch on timelines measured in quarters.

Which brings us back to the twenty-year-old in leg braces who sailed to America in 1931.

The Supply Side: When Coordination Gets Cheap

To understand what is happening on the supply side, I spoke with Sangeet Paul Choudary, author of Reshuffle. I asked him what most companies get wrong about AI. Everyone starts with tasks, he said. A lawyer drafts contracts faster. A marketer generates copy faster. A developer writes code faster. Fine. But that is still the same workflow.

The deep shift, he argues, comes from cutting the effort it takes to turn one team’s output into another team’s input. The meeting on your calendar because engineering and marketing speak different languages. The email chain because the CRM does not talk to the ERP. In Coase’s language, those frictions are transaction costs.

And AI’s biggest economic payoff comes from driving those transaction costs down to nearly zero.

When AI agents can negotiate terms, monitor quality, interpret documents, and reconcile outputs, firms can distribute work more widely, without losing the grip they once needed hierarchy to provide.

What does that look like in practice? It starts with what Choudary calls the atomic unit of work: the smallest piece of productive activity that can be separated and then assigned.

Take fashion. For Zara, the atomic unit was the collection: a coherent batch of designs that had to fit the brand, be manufacturable, and move fast enough to catch a trend. That required tightly coupled human judgment across design, sourcing, production, and logistics. So Zara built a supply chain around speed and coordination, with production close to Spain and fresh inventory moving out of La Coruña twice a week.

Then Shein kept shrinking the unit of work. A collection became a set of fragments. Then the fragments got smaller still, until what remained was a single design decision.

“The designer still exists,” Choudary told me. “But their creative bandwidth has been compressed to almost nothing.” Work that once sat with a designer who could hold manufacturing constraints, brand identity, and seasonal timing in mind can now be split into narrow prompts: Reference these three images. Draw a collar. Rework the cuff. Try a different hemline.

Human judgment still matters. But it shows up less. More of the intelligence now sits in the system that parcels out the work, recombines the pieces, and decides what deserves to scale.

In a cramped Guangzhou workshop, workers would hunch over sewing machines under hard fluorescent light, finish a piece, slide it into a turquoise bag, and toss it onto the pile. The system reacts to each signal as it arrives, from an Instagram click to an Amazon sale.

That helps explain why Gap or Under Armour struggle. They are still organized around the older unit of work: long cycles, big production runs, broad seasonal catalogs. Their unit is still too large.

You can see it in software, too. Adobe treated the file as the basic unit of design work. You work on the file. You pass the file around. Figma treated the element, the text block, the shared object, as the unit. Suddenly everyone is on the same canvas. Version reconciliation fades. Governance stops being something imposed after the fact and becomes part of the workflow itself. By the time Adobe recognized the threat, it was serious enough that the company attempted a $20 billion acquisition. Regulators blocked it.

So the pattern is consistent. The unit of work gets smaller. The pieces become more modular. Coordination gets cheaper. And once that happens, more of what once required a firm begins to look like something that can be orchestrated across a network instead.

Where Supply Meets Demand

The convergence matters because it changes the minimum viable size of a firm. When coordination gets cheap and demand gets weird, more businesses can exist at smaller scale.

Think YouTube channels versus TV shows. It took 150 people to make a TV show. Now 5 to 10 people with AI tools can run a wildly successful channel. The same explosion is coming to software. A software company used to require 10,000 customers, 50 employees, and $1 to $5 million in capital. But AI is threatening to drop those requirements to 500 customers, 2 people, and minimal funding.

That is why Wall Street repriced software companies so much. In early February 2026, software and services stocks shed roughly $830 billion in market value over six trading days. Salesforce, Adobe, ServiceNow all get hammered. The market realized that software barriers built on workflow lock-in will dissolve if AI agents can coordinate across tools without anyone agreeing on a standard.

None of this means large companies disappear. They never do. When e-commerce arrived, Sears collapsed, but Amazon rose in its place. The form changes. The scale persists.

So what does a big company look like after the Coasean Singularity?

How Large Organizations Survive (When They Do)

The honest answer is that most won’t in their current form. But there is an alternative, and it has a proof of concept. It is called Haier, the world’s No. 1 major-appliances brand for 17 years running.

In December 1984, a 35-year-old named Zhang Ruimin was sent to run a failing refrigerator factory in Qingdao. His predecessors had all quit. Annual turnover was 3.48 million yuan. The factory was losing 1.47 million. Workers urinated on the floor.

A few months later, a customer returned a faulty refrigerator. Zhang checked the inventory and found 76 defective units, about a fifth of the stock. He lined them up on the factory floor, handed workers sledgehammers, and told them to smash every one. Then he picked up a sledgehammer himself and brought it down on a refrigerator door. Each unit was worth four years’ wages. Some workers wept as they swung.

That sledgehammer now sits in Haier Group’s headquarters museum, beside the refrigerators and washing machines that came after it. But the sledgehammer was only the beginning. Over the next two decades, Zhang pulled apart the hierarchy itself, reorganizing more than 80,000 employees into over 4,000 self-managing micro-enterprises.

Each one operates like a startup. It owns its own profit and loss. It makes key decisions. It stays tied to a specific user need. Employees do not collect a fixed salary simply for showing up. Instead, their income rises or falls with the value they create for customers. A strong micro-enterprise earns its place and stays; a weak one does not.

Zhang saw the traditional enterprise as a ship. One captain, one direction, everyone on board. Fine for calm seas. But the seas were not calm. What he wanted was a rainforest: diverse, distributed, self-organizing, resilient because no single failure could bring the whole system down. So he broke the ship apart and let the pieces find their own currents.

One micro-enterprise leader said, “My wife used to complain that I didn’t come home from work until after 9:00 at night. But now she is very patient and proud about the hours I keep, because she knows I am building my own company and working for the benefit of our own family.” He paused. “And I am making my own decisions, not acting on the decisions someone else has made.”

When Haier acquired GE Appliances in 2016, GE’s market share in home appliances had languished around 2 percent for four years. Under the micro-enterprise model, it surged tenfold. Revenue more than doubled. Small teams swarmed opportunities the way a traditional hierarchy never could.

So why isn’t this just fragmentation? Why isn’t it 4,000 independent contractors with a logo?

Because when Haier operates as a platform, a kind of internal market with a shared brand and balance sheet, it does what a contract cannot. It provides accountability. It provides trust. It provides a brand, which in a world of infinite AI-generated noise is one of the few filters customers actually rely on. And it provides the capital to absorb failure.

“The task is not to turn Haier’s internal staff into entrepreneurs, but rather to attract all the entrepreneurs in society onto our platform,” Zhang says.

Most micro-enterprise bets lose. Only an entity with sufficient scale can sustain the portfolio of experiments required to find the ones that win.

The Question That Matters

I went back to Coase because I needed an anchor. Transaction costs are falling. The unit of work is shrinking. The middle of the market is thinning. An economy dominated by fragmented supply, splintered demand, and AI agents handling the coordination in between does not resemble anything most of us were trained to navigate.

All the while, the forces driving us toward the Coasean Singularity are too theoretically fundamental and too empirically visible to be a mirage.

My nephew is fourteen years old, living in New Zealand. When I think about the economy he will inherit, I do not think about which AI tool will be dominant. By the time he enters the workforce, “company” might mean something his father would not recognize. A temporary coordination pattern. A portfolio of bets. And “career” means portfolio.

If the micro-enterprise economy works only for the relentless, for the people who can treat career volatility as a lifestyle brand, then our economy is also a tournament.

And tournaments produce a few winners and a lot of wreckage.

The urgent question is how to position yourself. Still, the defining question is whether we can build institutions and shared norms strong enough to make this new economy socially durable and make it possible to live a decent life.

We have not yet passed the Coasean Singularity. Pay close attention to who is shaping the rules, and find a way into the conversation.

The window to shape what comes after is still open. Barely.